36. Time Series Data Analysis and Processing#

36.1. Introduction#

Time series is a data type often encountered in data analysis. Understanding and mastering relevant features and processing methods can help us handle time series analysis tasks. In this experiment, we focus on learning a series of preprocessing techniques for time series using Pandas.

36.2. Key Points#

Time generation

Time conversion

Time calculation

Time zone

Timestamp

Timestamp index

Time series retrieval

Time series offset

Resampling

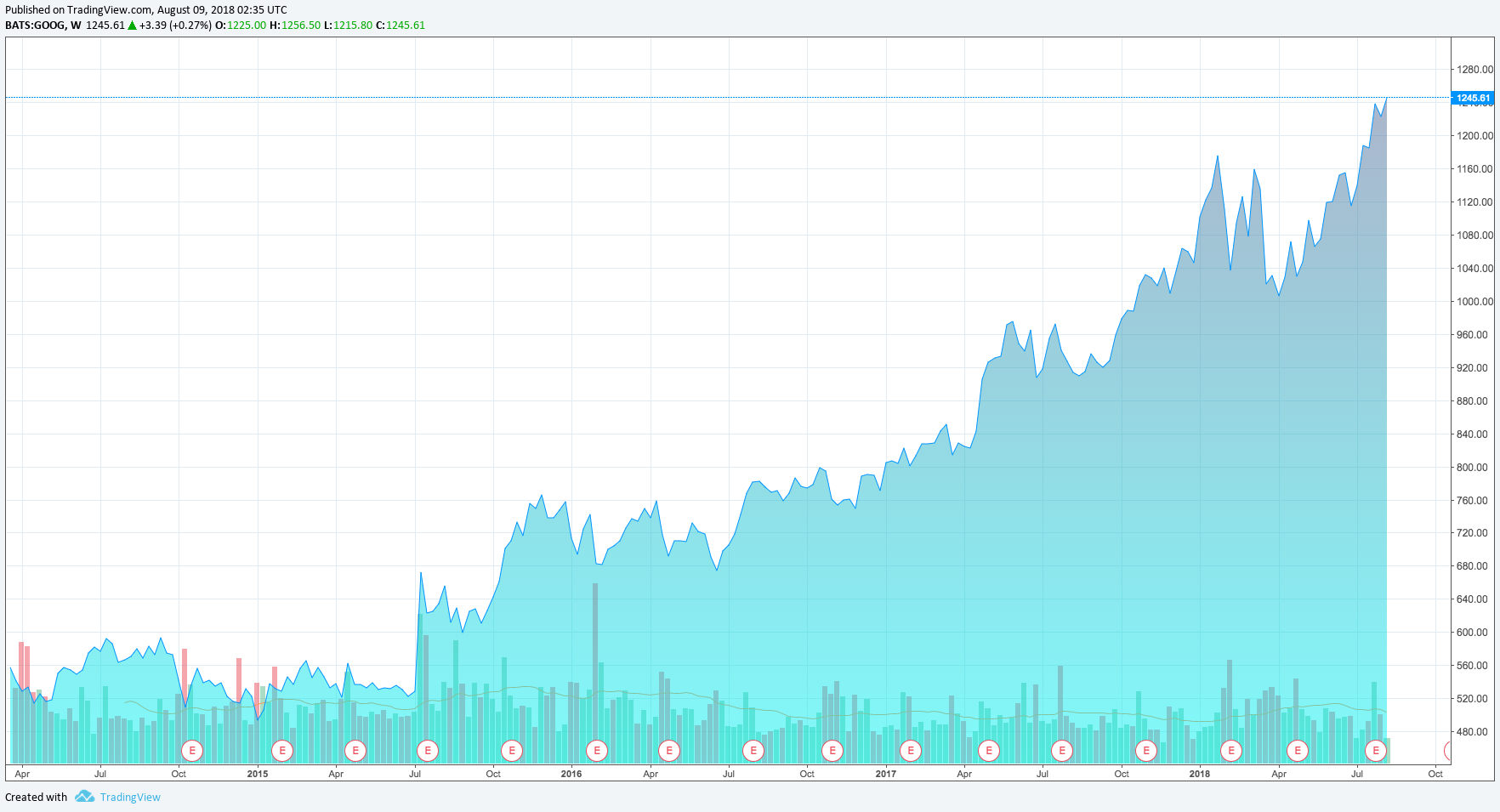

Time series analysis is often encountered in the process of data analysis, especially in financial data analysis. A time series is a set of random variables sorted by time. For example, the GDP or CPI index regularly released by the National Bureau of Statistics every year or month; the numerical changes of stocks, funds, and indexes over a period of time are all time series.

The following figure shows the stock price change curve of Google for only 5 years. In fact, this curve is drawn from the daily closing prices, which is a typical time series dataset.

In addition to the financial field, time series are widely present in other aspects such as the environment and physics. For example, the air quality index changes over time, and server log data is generated over time.

Similarly, Pandas provides a series of standard time series processing tools and algorithms, which are essential for processing and analyzing time series using Python. Next, we will learn about time generation, time series generation, indexing, slicing, sampling, etc.

36.3. Time Generation#

Before learning about time series, it is necessary to

understand time first. In Python, we usually use the

datetime

and

time

modules to perform time operations. For example,

datetime.datetime.now

can print the current time.

import datetime

datetime.datetime.now() # 获取当前时间

datetime.datetime(2023, 11, 11, 13, 36, 28, 1146)

As can be seen,

datetime.datetime.now()

returns a time object, which are in sequence: year, month,

day, hour, minute, second, and microsecond. Among them, the

value range of microsecond is

0

<=

microsecond

<

1000000. There is an equivalent method for

datetime.datetime.now(), which is

datetime.datetime.today().

datetime.datetime.today() # 获取当前时间

datetime.datetime(2023, 11, 11, 13, 36, 28, 15287)

You can choose to return only a part of the time.

datetime.datetime.now().year # 返回当前年份

2023

In addition to getting the current time, you can manually specify a time object.

datetime.datetime(2017, 10, 1, 10, 59, 30) # 指定任意时间

datetime.datetime(2017, 10, 1, 10, 59, 30)

36.4. Time Calculation#

datetime

time objects can be involved in calculations. For example,

adding a certain amount of time and years, calculating year

intervals, etc.

datetime.datetime(2018, 10, 1) - datetime.datetime(2017, 10, 1) # 计算时间间隔

datetime.timedelta(days=365)

As can be seen, the above returns a

datetime.timedelta

object.

timedelta

can be used to represent differences in time, but only up to

three units are retained, namely: days, seconds, and

milliseconds. For example:

datetime.datetime.now() - datetime.datetime(2017, 10, 1) # timedelta 表示间隔时间

datetime.timedelta(days=2232, seconds=48988, microseconds=37705)

Therefore, if you want to add one year to the current time, you need to convert the number of years into days for calculation.

datetime.datetime.now() + datetime.timedelta(365) # 需将年份转换为天

datetime.datetime(2024, 11, 10, 13, 36, 28, 41982)

36.5. Time Format Conversion#

Although

datetime

objects are precise, there are many times when we want to

convert them into custom time representation styles, such

as:

October

1,

2018, or

2018/10/1, etc. At this time, it is necessary to convert the

datetime

object into a string object.

We can use

datetime.date.strftime

to complete the conversion between time and string.

datetime.datetime.now().strftime("%Y-%m-%d") # 转换为自定义样式

'2023-11-11'

datetime.datetime.now().strftime("%Y 年 %m 月 %d 日") # 转换为自定义样式

'2023 年 11 月 11 日'

You will find that we have used placeholders. Then, the

placeholders supported by

strftime

are:

-

%yTwo-digit year representation (00 - 99) -

%YFour-digit year representation (0000 - 9999) -

%mMonth (01 - 12) -

%dDay of the month (0 - 31) -

%HHour in 24-hour format (0 - 23) -

%IHour in 12-hour format (01 - 12) -

%MMinutes (00 - 59) -

%SSeconds (00 - 59) -

%aLocal abbreviated weekday name -

%ALocal full weekday name -

%bLocal abbreviated month name -

%BLocal full month name -

%cLocal corresponding date and time representation -

%jDay of the year (001 - 366) -

%pLocal equivalent of A.M. or P.M. -

%UWeek number of the year (00 - 53), with Sunday as the start of the week -

%wWeekday (0 - 6), with Sunday as the start of the week -

%WWeek number of the year (00 - 53), with Monday as the start of the week -

%xLocal corresponding date representation -

%XLocal corresponding time representation -

%ZName of the current time zone

In addition to converting

datetime

objects to strings, you can also convert string time to

datetime

objects. This operation is mainly considered for the

flexibility of

datetime

objects, which can be used for secondary conversion. For

example, you only need to use placeholders to represent the

rules of the original string, and it can be automatically

converted into a

datetime

time object, which is very convenient.

datetime.datetime.strptime("2018-10-1", "%Y-%m-%d")

datetime.datetime(2018, 10, 1, 0, 0)

36.6. Time Zone#

A time zone is a definition of an area on Earth that uses the same time. If time is expressed in Coordinated Universal Time (UTC), then we can use the UTC offset to define the time in different time zones. For example, since Beijing is in the eighth time zone east of Greenwich, Beijing time is UTC +08:00, which represents a time zone that is 8 hours ahead of Coordinated Universal Time.

{kind=link}

When we use

datetime.now()

to print the current time, it does not contain time zone

information. This is also called a Naive datetime object,

that is, a “naive time zone”. We can use

datetime.datetime.utcnow()

to get the UTC time.

datetime.datetime.utcnow() # 获取 UTC 时间

datetime.datetime(2023, 11, 11, 5, 36, 28, 59689)

So, at this time, if you want to get Beijing time, you can add 8 hours to UTC, i.e., UTC+8:00.

utc = datetime.datetime.utcnow() # 获取 UTC 时间

tzutc_8 = datetime.timezone(datetime.timedelta(hours=8)) # + 8 小时

utc_8 = utc.astimezone(tzutc_8) # 添加到时区中

print(utc_8)

2023-11-11 05:36:28.063327+08:00

The time has been introduced above. If we associate the time with the collected data, a time series is formed. In a time series, there are mainly two types:

Timestamp: A single moment.

-

Time interval: Composed of a start timestamp and an end timestamp. Some time intervals can be a period, such as the year 2018, representing the time interval of the whole year.

Next, we learn the methods of using Pandas to process time series.

36.7. Timestamp#

A timestamp represents a specific point in time. In Pandas,

we can directly use

pandas.Timestamp

to create timestamps.

import pandas as pd

pd.Timestamp("2018-10-1")

Timestamp('2018-10-01 00:00:00')

Alternatively, create timestamps by combining with the

datetime

module.

pd.Timestamp(datetime.datetime.now())

Timestamp('2023-11-11 13:36:28.350028')

In addition, we can also use

pandas.to_datetime

to create timestamps. For example:

pd.to_datetime("1-10-2018")

Timestamp('2018-01-10 00:00:00')

The above code creates a timestamp for

2018-01-10

by default. What if we want it to be

2018-10-01? We can correct it by using the

dayfirst=True

parameter.

pd.to_datetime("1-10-2018", dayfirst=True)

Timestamp('2018-10-01 00:00:00')

36.8. DatetimeIndex for Time Index#

Timestamps are not the type that is often encountered in time series. If we have a data table sorted by time, then a more important data type is the DatetimeIndex. As the name implies, a time index consists of a series of timestamps, but in Pandas, the data type is DatetimeIndex.

We can also use

pd.to_datetime()

to create a time index. The difference from creating

timestamps above is that you only need to input a list

containing multiple moments.

pd.to_datetime(["2018-10-1", "2018-10-2", "2018-10-3"]) # 生成时间索引

DatetimeIndex(['2018-10-01', '2018-10-02', '2018-10-03'], dtype='datetime64[ns]', freq=None)

Of course, the Series and DataFrame in Pandas can also be

directly converted through

to_datetime.

s = pd.Series(["2018-10-1", "2018-10-2", "2018-10-3"])

pd.to_datetime(s) # 将 Seris 中字符串转换为时间

0 2018-10-01

1 2018-10-02

2 2018-10-03

dtype: datetime64[ns]

It is worth noting here that the time in the original Series

is a string, and after conversion by

pd.to_datetime(), it becomes a

datetime64

time. However, it is not a time index in the strict sense. A

time index requires placing it in the index position of the

Series or DataFrame. For example:

pd.Series(index=pd.to_datetime(s)).index # 当时间位于索引时,就是 DatetimeIndex

DatetimeIndex(['2018-10-01', '2018-10-02', '2018-10-03'], dtype='datetime64[ns]', freq=None)

Now what we see is the DatetimeIndex type.

In fact, another more commonly used method to generate a

DatetimeIndex is

pandas.date_range. We can specify rules to let

pandas.date_range

generate an ordered DatetimeIndex.

The default parameters of the

date_range

method are as follows:

pandas.date_range(start=None, end=None, periods=None, freq=’D’, tz=None, normalize=False, name=None, closed=None, **kwargs)

Among them:

-

start=:Sets the start time -

end=:Sets the end time -

periods=:Sets the time interval. IfNone, the start and end times need to be set separately. -

freq=:Sets the interval period. -

tz=:Sets the time zone.

In particular, the

freq=

frequency parameter is very crucial. The available periods

that can be set are:

-

freq='s': Seconds -

freq='min': Minutes -

freq='H': Hours -

freq='D': Days -

freq='w': Weeks -

freq='m': Months -

freq='BM': Last day of each month -

freq='W': Sundays of each week

pd.date_range("2018-10-1", "2018-10-2", freq="H") # 按小时间隔生成时间索引

DatetimeIndex(['2018-10-01 00:00:00', '2018-10-01 01:00:00',

'2018-10-01 02:00:00', '2018-10-01 03:00:00',

'2018-10-01 04:00:00', '2018-10-01 05:00:00',

'2018-10-01 06:00:00', '2018-10-01 07:00:00',

'2018-10-01 08:00:00', '2018-10-01 09:00:00',

'2018-10-01 10:00:00', '2018-10-01 11:00:00',

'2018-10-01 12:00:00', '2018-10-01 13:00:00',

'2018-10-01 14:00:00', '2018-10-01 15:00:00',

'2018-10-01 16:00:00', '2018-10-01 17:00:00',

'2018-10-01 18:00:00', '2018-10-01 19:00:00',

'2018-10-01 20:00:00', '2018-10-01 21:00:00',

'2018-10-01 22:00:00', '2018-10-01 23:00:00',

'2018-10-02 00:00:00'],

dtype='datetime64[ns]', freq='H')

# 从 2018-10-1 开始,以天为间隔,向后推 10 次

pd.date_range("2018-10-1", periods=10, freq="D")

DatetimeIndex(['2018-10-01', '2018-10-02', '2018-10-03', '2018-10-04',

'2018-10-05', '2018-10-06', '2018-10-07', '2018-10-08',

'2018-10-09', '2018-10-10'],

dtype='datetime64[ns]', freq='D')

# 从 2018-10-1 开始,以 1H20min 为间隔,向后推 10 次

pd.date_range("2018-10-1", periods=10, freq="1H20min")

DatetimeIndex(['2018-10-01 00:00:00', '2018-10-01 01:20:00',

'2018-10-01 02:40:00', '2018-10-01 04:00:00',

'2018-10-01 05:20:00', '2018-10-01 06:40:00',

'2018-10-01 08:00:00', '2018-10-01 09:20:00',

'2018-10-01 10:40:00', '2018-10-01 12:00:00'],

dtype='datetime64[ns]', freq='80T')

With

date_range, we can generate any time index that changes according to

a certain pattern.

Previously, we learned that

timedelta

can be used for time operations. In a DatetimeIndex, we can

use offset objects to make more flexible changes to the

timestamp index. For example:

-

It is possible to increase or decrease the time index by a certain time period.

-

It is possible to multiply the time index by an integer.

-

It is possible to move the time index forward or backward to the next or previous specific offset date.

time_index = pd.date_range("2018-10-1", periods=10, freq="1D1H")

time_index

DatetimeIndex(['2018-10-01 00:00:00', '2018-10-02 01:00:00',

'2018-10-03 02:00:00', '2018-10-04 03:00:00',

'2018-10-05 04:00:00', '2018-10-06 05:00:00',

'2018-10-07 06:00:00', '2018-10-08 07:00:00',

'2018-10-09 08:00:00', '2018-10-10 09:00:00'],

dtype='datetime64[ns]', freq='25H')

Use the offset object to increase

time_index

by 1 month + 2 days + 3 hours in sequence.

from pandas import offsets

time_index + offsets.DateOffset(months=1, days=2, hours=3)

DatetimeIndex(['2018-11-03 03:00:00', '2018-11-04 04:00:00',

'2018-11-05 05:00:00', '2018-11-06 06:00:00',

'2018-11-07 07:00:00', '2018-11-08 08:00:00',

'2018-11-09 09:00:00', '2018-11-10 10:00:00',

'2018-11-11 11:00:00', '2018-11-12 12:00:00'],

dtype='datetime64[ns]', freq=None)

Alternatively, use the offset object to offset

time_index

backward by 2 weeks.

time_index + 2 * offsets.Week()

DatetimeIndex(['2018-10-15 00:00:00', '2018-10-16 01:00:00',

'2018-10-17 02:00:00', '2018-10-18 03:00:00',

'2018-10-19 04:00:00', '2018-10-20 05:00:00',

'2018-10-21 06:00:00', '2018-10-22 07:00:00',

'2018-10-23 08:00:00', '2018-10-24 09:00:00'],

dtype='datetime64[ns]', freq=None)

In addition to

offsets.DateOffset

and

offsets.Week

mentioned in the example, the commonly used offsets objects

also include:

|

DateOffset Name |

Description |

|---|---|

DateOffset |

Custom, default is one week |

BDay |

Business day |

CDay |

Custom business day |

MonthEnd |

End of month |

QuarterEnd |

End of quarter |

YearEnd |

End of year |

A more detailed form of DateOffset Objects can be read in the official documentation.

You can find that the DateOffset object is very flexible. With a little combination, you can achieve any desired time offset result. In fact, the DateOffset object is not only valid for DatetimeIndex, but also can be operated on the timestamp Timestamp. This should be easy to understand, as the DatetimeIndex is equivalent to an extension of the Timestamp.

36.9. Time Intervals (Periods)#

Above, we have a relatively thorough understanding of both the Timestamp and the DatetimeIndex. In addition, there are also the Period time interval and PeriodIndex time interval index objects in Pandas. What are Periods? For example: days, months, quarters, years.

# 1 年跨度

pd.Period("2018")

Period('2018', 'A-DEC')

# 1 个月跨度

pd.Period("2018-1")

Period('2018-01', 'M')

# 1 天跨度

pd.Period("2018-1-1")

Period('2018-01-01', 'D')

You will see that there is a letter after each time

interval. In fact, this is the

freq=

frequency corresponding to the time interval. You may be

thinking that Periods seems to have no difference from the

above Timestamp. Then let’s regenerate a Timestamp to take a

look.

pd.Timestamp("2018-1-1")

Timestamp('2018-01-01 00:00:00')

At this point, you should be able to notice the difference

between Timestamp and Periods. Periods represents the entire

day of

2018-01-01, while Timestamp only represents the moment of

2018-01-01

00:00:00.

36.10. PeriodsIndex (Time Interval Index)#

Similar to “timestamp → time index”, time intervals also

correspond to the PeriodsIndex (time interval index). And we

can generate an index sequence through the

pandas.period_range()

method.

p = pd.period_range("2018", "2019", freq="M") # 生成 2018-1 到 2019-1 序列,按月分布

p

PeriodIndex(['2018-01', '2018-02', '2018-03', '2018-04', '2018-05', '2018-06',

'2018-07', '2018-08', '2018-09', '2018-10', '2018-11', '2018-12',

'2019-01'],

dtype='period[M]')

When generating the index sequence, it is necessary to

specify the

freq=

frequency, which is similar to generating the DatetimeIndex

above. At the same time, we can use

asfreq

to reset the frequency.

p.asfreq(freq="D", how="S") # 频度从 M → D

PeriodIndex(['2018-01-01', '2018-02-01', '2018-03-01', '2018-04-01',

'2018-05-01', '2018-06-01', '2018-07-01', '2018-08-01',

'2018-09-01', '2018-10-01', '2018-11-01', '2018-12-01',

'2019-01-01'],

dtype='period[D]')

Here,

how=S

represents the first day of each month (Start), and it can

also be set to

how=E

(End).

36.11. Selection, Slicing, and Shifting of Time Series Data#

You may be wondering why Pandas uses timestamps, time indexes, time intervals, etc. In fact, these basic data types emerged to facilitate our operations on time series data. With Timestamp and Periods, we can complete operations such as data selection, slicing, as well as more complex combined transformations like shifting and resampling.

Next, we will try to generate an example of a Series with a time index and select data from it.

import numpy as np

timeindex = pd.date_range("2018-1-1", periods=20, freq="M")

s = pd.Series(np.random.randn(len(timeindex)), index=timeindex)

s

2018-01-31 0.330330

2018-02-28 1.087339

2018-03-31 -1.486658

2018-04-30 0.783250

2018-05-31 1.527258

2018-06-30 0.152985

2018-07-31 -0.310307

2018-08-31 -0.839569

2018-09-30 -1.905840

2018-10-31 0.542714

2018-11-30 -0.083846

2018-12-31 0.330400

2019-01-31 -0.475228

2019-02-28 -0.871950

2019-03-31 -1.174331

2019-04-30 0.095896

2019-05-31 0.353876

2019-06-30 0.159181

2019-07-31 0.759272

2019-08-31 -1.708107

Freq: M, dtype: float64

Select all the data for the year 2018.

s["2018"]

2018-01-31 0.330330

2018-02-28 1.087339

2018-03-31 -1.486658

2018-04-30 0.783250

2018-05-31 1.527258

2018-06-30 0.152985

2018-07-31 -0.310307

2018-08-31 -0.839569

2018-09-30 -1.905840

2018-10-31 0.542714

2018-11-30 -0.083846

2018-12-31 0.330400

Freq: M, dtype: float64

Select all the data between July 2018 and March 2019.

s["2018-07":"2019-03"]

2018-07-31 -0.310307

2018-08-31 -0.839569

2018-09-30 -1.905840

2018-10-31 0.542714

2018-11-30 -0.083846

2018-12-31 0.330400

2019-01-31 -0.475228

2019-02-28 -0.871950

2019-03-31 -1.174331

Freq: M, dtype: float64

In addition to querying and slicing, we can also use the Shifting method to shift the time index as a whole.

s.shift(3) # 时间索引以默认 Freq: M 向后偏移 3 个单位

2018-01-31 NaN

2018-02-28 NaN

2018-03-31 NaN

2018-04-30 0.330330

2018-05-31 1.087339

2018-06-30 -1.486658

2018-07-31 0.783250

2018-08-31 1.527258

2018-09-30 0.152985

2018-10-31 -0.310307

2018-11-30 -0.839569

2018-12-31 -1.905840

2019-01-31 0.542714

2019-02-28 -0.083846

2019-03-31 0.330400

2019-04-30 -0.475228

2019-05-31 -0.871950

2019-06-30 -1.174331

2019-07-31 0.095896

2019-08-31 0.353876

Freq: M, dtype: float64

You can understand the above process as shifting the time

index backward (into the future) by 3 units, and Pandas will

automatically fill the missing data with NaN. In addition,

you can also specify the

freq=

parameter to determine the unit size of the shift.

s.shift(-3, freq="D") # 时间索引以 Freq: D 向前偏移 3 个单位

2018-01-28 0.330330

2018-02-25 1.087339

2018-03-28 -1.486658

2018-04-27 0.783250

2018-05-28 1.527258

2018-06-27 0.152985

2018-07-28 -0.310307

2018-08-28 -0.839569

2018-09-27 -1.905840

2018-10-28 0.542714

2018-11-27 -0.083846

2018-12-28 0.330400

2019-01-28 -0.475228

2019-02-25 -0.871950

2019-03-28 -1.174331

2019-04-27 0.095896

2019-05-28 0.353876

2019-06-27 0.159181

2019-07-28 0.759272

2019-08-28 -1.708107

dtype: float64

36.12. Resampling of Time Series Data#

Resampling is an operation often used in the processing of time series data. The purpose of resampling is to increase or decrease the frequency of a time-indexed sequence. For example: when the volume of time series data is very large, we can obtain a new dataset with a smaller scale but still relatively comprehensive time coverage through the method of low-frequency sampling. In addition, resampling can be a very important means when data alignment is required for multiple datasets with different frequencies.

Similarly, initialize a sample Series.

dateindex = pd.period_range("2018-10-1", periods=20, freq="D")

s = pd.Series(np.random.randn(len(dateindex)), index=dateindex)

s

2018-10-01 -0.375011

2018-10-02 1.052191

2018-10-03 -0.232303

2018-10-04 -1.632577

2018-10-05 -0.362599

2018-10-06 -0.866722

2018-10-07 -0.244350

2018-10-08 1.501014

2018-10-09 0.558769

2018-10-10 -2.173344

2018-10-11 0.112917

2018-10-12 2.078360

2018-10-13 1.596991

2018-10-14 -0.098130

2018-10-15 -0.175248

2018-10-16 0.184979

2018-10-17 -0.223399

2018-10-18 0.427384

2018-10-19 0.170283

2018-10-20 -0.234324

Freq: D, dtype: float64

Next, we downsample the Series by 2 days and sum the data

corresponding to the 2 days as the new data. Note that when

performing downsampling using

pandas.DataFrame.resample, a calculation method (sum, average, maximum, minimum,

etc.) needs to be selected.

s.resample("2D").sum() # 降采样,并将删去的数据依次合并到保留数据中

2018-10-01 0.677181

2018-10-03 -1.864881

2018-10-05 -1.229321

2018-10-07 1.256664

2018-10-09 -1.614575

2018-10-11 2.191277

2018-10-13 1.498861

2018-10-15 0.009731

2018-10-17 0.203986

2018-10-19 -0.064040

Freq: 2D, dtype: float64

Well, if you don’t want to operate on the data corresponding

to the data index during downsampling, but only retain the

data corresponding to the original timestamps, you can use

the

.asfreq()

method.

s.resample("2D").asfreq() # 降采样,直接舍去数据

2018-10-01 -0.375011

2018-10-03 -0.232303

2018-10-05 -0.362599

2018-10-07 -0.244350

2018-10-09 0.558769

2018-10-11 0.112917

2018-10-13 1.596991

2018-10-15 -0.175248

2018-10-17 -0.223399

2018-10-19 0.170283

Freq: 2D, dtype: float64

It can also be done like this. Downsample by 2 days and list

the original values, maximum values, minimum values, etc. of

the data corresponding to the 2 days. This method is mainly

used in stock analysis, where

open,

high,

low, and

close

correspond to the opening price, highest price, lowest

price, and closing price during the stock trading process.

s.resample("2D").ohlc()

| open | high | low | close | |

|---|---|---|---|---|

| 2018-10-01 | -0.375011 | 1.052191 | -0.375011 | 1.052191 |

| 2018-10-03 | -0.232303 | -0.232303 | -1.632577 | -1.632577 |

| 2018-10-05 | -0.362599 | -0.362599 | -0.866722 | -0.866722 |

| 2018-10-07 | -0.244350 | 1.501014 | -0.244350 | 1.501014 |

| 2018-10-09 | 0.558769 | 0.558769 | -2.173344 | -2.173344 |

| 2018-10-11 | 0.112917 | 2.078360 | 0.112917 | 2.078360 |

| 2018-10-13 | 1.596991 | 1.596991 | -0.098130 | -0.098130 |

| 2018-10-15 | -0.175248 | 0.184979 | -0.175248 | 0.184979 |

| 2018-10-17 | -0.223399 | 0.427384 | -0.223399 | 0.427384 |

| 2018-10-19 | 0.170283 | 0.170283 | -0.234324 | -0.234324 |

In addition to downsampling, upsampling is also feasible. However, when considering upsampling, what should we do about the values corresponding to the timestamps newly added to the time index? Should we use the adjacent data or fill it with other methods?

For example, we can increase the time frequency from days to hours and fill the newly added rows with the same data.

s.resample("H").ffill() # 升采样,使用相同的数据对新增加行填充

2018-10-01 00:00 -0.375011

2018-10-01 01:00 -0.375011

2018-10-01 02:00 -0.375011

2018-10-01 03:00 -0.375011

2018-10-01 04:00 -0.375011

...

2018-10-20 19:00 -0.234324

2018-10-20 20:00 -0.234324

2018-10-20 21:00 -0.234324

2018-10-20 22:00 -0.234324

2018-10-20 23:00 -0.234324

Freq: H, Length: 480, dtype: float64

Control the maximum number of fillings by setting

limit=, and the values that are not filled will be automatically

marked as NaN.

s.resample("H").ffill(limit=3) # 升采样,最多填充临近 3 行

2018-10-01 00:00 -0.375011

2018-10-01 01:00 -0.375011

2018-10-01 02:00 -0.375011

2018-10-01 03:00 -0.375011

2018-10-01 04:00 NaN

...

2018-10-20 19:00 NaN

2018-10-20 20:00 NaN

2018-10-20 21:00 NaN

2018-10-20 22:00 NaN

2018-10-20 23:00 NaN

Freq: H, Length: 480, dtype: float64

36.13. Time Series Data Time Zone Processing#

Above, we learned about time zone processing in datetime, and time zone processing may also occur in Pandas. Similar to datetime, the time series in Pandas is still naive in terms of time zone.

naive_time = pd.date_range("1/10/2018 9:00", periods=10, freq="D")

naive_time

DatetimeIndex(['2018-01-10 09:00:00', '2018-01-11 09:00:00',

'2018-01-12 09:00:00', '2018-01-13 09:00:00',

'2018-01-14 09:00:00', '2018-01-15 09:00:00',

'2018-01-16 09:00:00', '2018-01-17 09:00:00',

'2018-01-18 09:00:00', '2018-01-19 09:00:00'],

dtype='datetime64[ns]', freq='D')

Therefore, when we need to convert to local time, we need to first add UTC time zone information to the time series and then convert it to local time.

utc_time = naive_time.tz_localize("UTC")

utc_time

DatetimeIndex(['2018-01-10 09:00:00+00:00', '2018-01-11 09:00:00+00:00',

'2018-01-12 09:00:00+00:00', '2018-01-13 09:00:00+00:00',

'2018-01-14 09:00:00+00:00', '2018-01-15 09:00:00+00:00',

'2018-01-16 09:00:00+00:00', '2018-01-17 09:00:00+00:00',

'2018-01-18 09:00:00+00:00', '2018-01-19 09:00:00+00:00'],

dtype='datetime64[ns, UTC]', freq='D')

Next, we use the

tz_localize

method to achieve time zone conversion.

utc_time.tz_convert("Asia/Shanghai")

DatetimeIndex(['2018-01-10 17:00:00+08:00', '2018-01-11 17:00:00+08:00',

'2018-01-12 17:00:00+08:00', '2018-01-13 17:00:00+08:00',

'2018-01-14 17:00:00+08:00', '2018-01-15 17:00:00+08:00',

'2018-01-16 17:00:00+08:00', '2018-01-17 17:00:00+08:00',

'2018-01-18 17:00:00+08:00', '2018-01-19 17:00:00+08:00'],

dtype='datetime64[ns, Asia/Shanghai]', freq='D')

Note that generally when we define

UTC+8:00, we use

Asia/Chongqing

or

Asia/Shanghai, not

Asia/Beijing. This is due to historical reasons.

In fact, when generating timestamps or time indices, you can

specify the

tz=

parameter to define the UTC time zone.

pd.date_range("1/10/2018 9:00", periods=10, freq="D", tz="Asia/Shanghai")

DatetimeIndex(['2018-01-10 09:00:00+08:00', '2018-01-11 09:00:00+08:00',

'2018-01-12 09:00:00+08:00', '2018-01-13 09:00:00+08:00',

'2018-01-14 09:00:00+08:00', '2018-01-15 09:00:00+08:00',

'2018-01-16 09:00:00+08:00', '2018-01-17 09:00:00+08:00',

'2018-01-18 09:00:00+08:00', '2018-01-19 09:00:00+08:00'],

dtype='datetime64[ns, Asia/Shanghai]', freq='D')

However, it should be noted that due to the change in the

reference of UTC time (tz=

will take the specified time as UTC), the result of the

previous line is different from the conversion result

through

tz_convert

before.

36.14. Summary#

A time series is nothing but a series of data sampled at time points, with a simple form. In this experiment, we learned about the basic elements of time series data in Pandas and the methods and techniques for Pandas to handle time series data. Only by mastering these methods can we better work with time series data and extract valuable information from it.